There are many small and medium size businesses that use real estate assets in their business as an office, warehouse or distribution facility. That is according to Joseph Ori, executive managing director of Paramount Capital Corp. He tells GlobeSt.com that if these small businesses lease an office building of at least 5,000 square feet, there is an interesting real estate structure for the company executives to own the building and net lease it to the operating company. He details this structure in the exclusive commentary below and says that the structure can generate real estate profits for the executive group and also limit and reduce the tax liability of the operating company.

The views expressed below are Ori's own.

This structure will be analyzed with the following data:

10,000 sq. ft. office building that is available for sale for $3 million or $300 per sq. ft.

An operating company that is a professional service entity named, Consulting LLC (CLLC) and 100% owned by the executive group will lease the entire building for its business.

Market office rents on a triple net basis are $20 per sq. ft., however, the rent will be set above market at $25 per sq. ft., for an annual rent of $250,000 (10,000 x $25/sq. ft.).

The executive group forms a limited liability company, ACME, LLC, to acquire and own the building for $3 million.

The building acquisition will be financed with a 10-year loan of $2 million at 5% interest and 25-year amortization.

The executive group will invest $1 million in equity in the building purchase.

CLLC is a consulting firm with revenue of $5 million, income before the lease expense of $300,000 and an EBITDA before lease expense of $350,000.

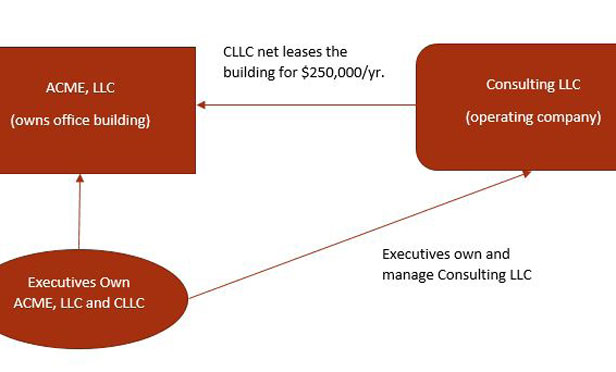

The executive group will form ACME, LLC, to buy the building for $3 million and finance it with a $2 million loan and $1 million of equity. The operating company, CLLC, will net lease the building for the market rent of $25/sq. ft. or an annual rent of $250,000. Since CLLC has an EBITDA of $350,000, it has ample free cash flow to pay the rent on the building. A flow chart of the structure of this transaction is as follows.

ACME, LLC will receive the annual net rent of $250,000 and pay the annual principal and interest on the $2 million loan of $140,302, which leaves a cash flow after debt of $115,302. The executives of CLLC who invested the $1 million in ACME, LLC, will receive a distribution of the $115,302, for a 11.5% return on their equity investment. CLLC has an income before the lease payment of $300,000 and will deduct the $250,000 lease payment and generate a distributable income of only $50,000 to the executive owners.

This structure substantially reduces the income of CLLC and hence the taxable income that flows through the entity to the executive owners personally and shifts much of the cash flow to ACME, LLC, the property owner. The executives who own CLLC and ACME benefit in a number of ways with this transaction as follows:

The taxable income in CLLC that will flow through to them in the LLC structure is substantially reduced

Ordinary income from CLLC has been converted into nontaxable cash distributions from ACME

Ordinary income from CLLC has been converted into capital gain upon sale of the building by ACME

Earn a high cash return of 11.5% on their equity in ACME

Profit from the future value increase in the office building

This type of transaction can be structured in a myriad of ways to meet the objectives of the executive group. In the example above, the annual rent was set at a high level to reduce the taxable income of the operating company, CLLC, through lease deductions and increase the cash flow to ACME. In other cases, the executive group may charge a lower rent to CLLC, to increase its profits and cash flow, while lowering the return to the building owner, ACME. Any small business owner, especially ones in professional services like lawyers, accountants, consultants, real estate brokers and investment firms should consider this structure for a headquarters building. They can become CRE owners and benefit from its tax advantages and appreciation and lower the taxable income for their operating company.

There are many small and medium size businesses that use real estate assets in their business as an office, warehouse or distribution facility. That is according to Joseph Ori, executive managing director of Paramount Capital Corp. He tells GlobeSt.com that if these small businesses lease an office building of at least 5,000 square feet, there is an interesting real estate structure for the company executives to own the building and net lease it to the operating company. He details this structure in the exclusive commentary below and says that the structure can generate real estate profits for the executive group and also limit and reduce the tax liability of the operating company.

The views expressed below are Ori's own.

This structure will be analyzed with the following data:

10,000 sq. ft. office building that is available for sale for $3 million or $300 per sq. ft.

An operating company that is a professional service entity named, Consulting LLC (CLLC) and 100% owned by the executive group will lease the entire building for its business.

Market office rents on a triple net basis are $20 per sq. ft., however, the rent will be set above market at $25 per sq. ft., for an annual rent of $250,000 (10,000 x $25/sq. ft.).

The executive group forms a limited liability company, ACME, LLC, to acquire and own the building for $3 million.

The building acquisition will be financed with a 10-year loan of $2 million at 5% interest and 25-year amortization.

The executive group will invest $1 million in equity in the building purchase.

CLLC is a consulting firm with revenue of $5 million, income before the lease expense of $300,000 and an EBITDA before lease expense of $350,000.

The executive group will form ACME, LLC, to buy the building for $3 million and finance it with a $2 million loan and $1 million of equity. The operating company, CLLC, will net lease the building for the market rent of $25/sq. ft. or an annual rent of $250,000. Since CLLC has an EBITDA of $350,000, it has ample free cash flow to pay the rent on the building. A flow chart of the structure of this transaction is as follows.

ACME, LLC will receive the annual net rent of $250,000 and pay the annual principal and interest on the $2 million loan of $140,302, which leaves a cash flow after debt of $115,302. The executives of CLLC who invested the $1 million in ACME, LLC, will receive a distribution of the $115,302, for a 11.5% return on their equity investment. CLLC has an income before the lease payment of $300,000 and will deduct the $250,000 lease payment and generate a distributable income of only $50,000 to the executive owners.

This structure substantially reduces the income of CLLC and hence the taxable income that flows through the entity to the executive owners personally and shifts much of the cash flow to ACME, LLC, the property owner. The executives who own CLLC and ACME benefit in a number of ways with this transaction as follows:

The taxable income in CLLC that will flow through to them in the LLC structure is substantially reduced

Ordinary income from CLLC has been converted into nontaxable cash distributions from ACME

Ordinary income from CLLC has been converted into capital gain upon sale of the building by ACME

Earn a high cash return of 11.5% on their equity in ACME

Profit from the future value increase in the office building

This type of transaction can be structured in a myriad of ways to meet the objectives of the executive group. In the example above, the annual rent was set at a high level to reduce the taxable income of the operating company, CLLC, through lease deductions and increase the cash flow to ACME. In other cases, the executive group may charge a lower rent to CLLC, to increase its profits and cash flow, while lowering the return to the building owner, ACME. Any small business owner, especially ones in professional services like lawyers, accountants, consultants, real estate brokers and investment firms should consider this structure for a headquarters building. They can become CRE owners and benefit from its tax advantages and appreciation and lower the taxable income for their operating company.

Continue Reading for Free

Register and gain access to:

- Breaking commercial real estate news and analysis, on-site and via our newsletters and custom alerts

- Educational webcasts, white papers, and ebooks from industry thought leaders

- Critical coverage of the property casualty insurance and financial advisory markets on our other ALM sites, PropertyCasualty360 and ThinkAdvisor

Already have an account? Sign In Now

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.

Natalie Dolce

Natalie Dolce, editor-in-chief of GlobeSt.com and GlobeSt. Real Estate Forum, is responsible for working with editorial staff, freelancers and senior management to help plan the overarching vision that encompasses GlobeSt.com, including short-term and long-term goals for the website, how content integrates through the company’s other product lines and the overall quality of content. Previously she served as national executive editor and editor of the West Coast region for GlobeSt.com and Real Estate Forum, and was responsible for coverage of news and information pertaining to that vital real estate region. Prior to moving out to the Southern California office, she was Northeast bureau chief, covering New York City for GlobeSt.com. Her background includes a stint at InStyle Magazine, and as managing editor with New York Press, an alternative weekly New York City paper. In her career, she has also covered a variety of beats for M magazine, Arthur Frommer's Budget Travel, FashionLedge.com, and Co-Ed magazine. Dolce has also freelanced for a number of publications, including MSNBC.com and Museums New York magazine.