|

|

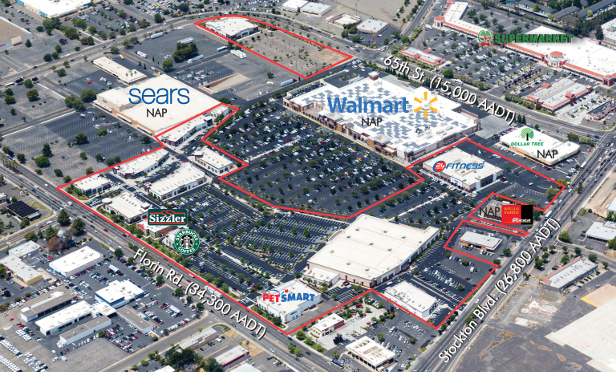

IRVINE, CA—Many power centers house dominant retailers that are still healthy performers within their respective categories—many of which are still categorized as investment grade, REZA Investment Group Inc.'s managing director Ramez Barsoum tells GlobeSt.com. The firm recently sold four retail power centers totaling more than 664,000 square feet: Florin Towne Centre, a 267,010-square-foot, open-air power center in Sacramento anchored by a 213,455-square-foot Walmart Supercenter; Redwood Gateway, an approximately 158,473-square-foot, institutional-quality community shopping center in Petaluma, CA, anchored by Kohl's, Michael's and Tuesday Morning; Mohave Crossroads, an approximately 182,168-square-foot center in Bullhead City, AZ, anchored by Target and Kohl's; and Laveen Village Marketplace, an institutional-quality community shopping center anchored by Fry's Food & Drug and Home Depot that encompasses approximately 282,400 square feet of retail space in the Phoenix submarket of Laveen, AZ.

We spoke with Barsoum about REZA's disposition strategy for power centers and what investors are looking for in these properties.

|

|

GlobeSt.com: What is your firm's strategy in handling the disposition of power centers for your clients?

Barsoum: Our team's business philosophy and approach have always been relationship centric, whereby we establish deep-rooted and long-term relationships with our clients. This results in collaborative marketing efforts where we engage with our client as a partner working toward the same goal. I mention this because the recent volatility within the retail sector, and notably with the tenant base that resides in power centers, has contributed to a more challenging environment in which to sell power centers.

First and foremost, we carefully assess the collateral; despite the recent narrative in the media propagating the demise of retail, property fundamentals are still paramount to an asset's performance. This assessment includes, but is not limited to, the asset's location and positioning within a market/submarket and any corresponding demographic trending in the area that the shopping center serves, the strength and financial wherewithal of the underlying tenancy, the tenant sales performance and trending within the property and the going-forward strategy of the collateral's tenant base. How are the tenants competitively positioned, and what current and future competitive threats may erode their market share moving forward?

In addition, with power centers, a careful assessment of the embedded co-tenancy clauses is critical. The potential impact of any “weak links” and the corresponding downside/erosion of NOI are important to address up front, since the prospective investor pool will evaluate these scenarios carefully and adjust their underwriting accordingly.

GlobeSt.com: What are power-center investors looking for in the properties they acquire?

Barsoum: Although there has been a great deal of negative publicity of late surrounding the retail asset category and retail tenants, there are still a number of tenants and categories that continue to thrive in the current market environment. In our opinion, some of the negative publicity has been overblown.

Retail, by nature, is constantly evolving, with new concepts that appeal to the consumer's evolving preferences and spending patterns replacing older retailers that may be heading toward the end of their life cycle. This has always been and will continue to be the nature of retail. Investors still value and place a premium on dominant locations in primary markets. To that end, we are not seeing a marked softening in power-center pricing in these “core” markets. However, we are observing upward pressure on capitalization rates with power centers in secondary markets/locations.

Beyond location, investors evaluate the strength of the tenancy within the collateral, their going-in basis in an asset (i.e., where rent structures are relative to current market rates in the event of a rollover/re-tenanting scenario) and, as previously mentioned, an understanding of co-tenancy implications and the corresponding effect on the property's income stream.

GlobeSt.com: How do you view the power-center market?

Barsoum: We believe that there are absolutely opportunities for investors to realize strong risk-adjusted returns in acquiring power centers in the current market environment. There are still many well-performing assets within this category, which are occupied by tenants who are continually evolving their business models to remain competitive and to thwart current and future competitive threats. Many power centers house dominant retailers that are still healthy performers within their respective categories, many of which are still categorized as investment grade.

GlobeSt.com: What else should our readers know about these last four dispositions?

Barsoum: Our team recently handled the sale of four power centers in separate transactions, each of which was unique and presented its own challenges/hurdles. One common theme across these four assets was the buyer profile. Specifically, we're seeing private equity in the form of high-net-worth individuals/family trusts, syndications, private entities with joint-venture equity investment partners and other non-institutional investors being the most active investors within this space, especially in secondary markets. The upward pressure on cap rates in secondary markets, combined with continued liquidity in the capital markets, has created an environment where these investors are able to achieve attractive risk-adjusted returns.

Within core markets, the assets in dominant locations are still generating interest from institutional equity, including REITs, pension funds and privately held large real estate platforms

Want to continue reading?

Become a Free ALM Digital Reader.

Once you are an ALM Digital Member, you’ll receive:

- Breaking commercial real estate news and analysis, on-site and via our newsletters and custom alerts

- Educational webcasts, white papers, and ebooks from industry thought leaders

- Critical coverage of the property casualty insurance and financial advisory markets on our other ALM sites, PropertyCasualty360 and ThinkAdvisor

Already have an account? Sign In Now

*May exclude premium content© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.

Carrie Rossenfeld

Carrie Rossenfeld is a reporter for the San Diego and Orange County markets on GlobeSt.com and a contributor to Real Estate Forum. She was a trade-magazine and newsletter editor in New York City before moving to Southern California to become a freelance writer and editor for magazines, books and websites. Rossenfeld has written extensively on topics including commercial real estate, running a medical practice, intellectual-property licensing and giftware. She has edited books about profiting from real estate and has ghostwritten a book about starting a home-based business.