NEWPORT BEACH, CA—The single-family rental sector, a newly institutionalized property type, is less well known and more fragmented than other sectors. The vast majority of single-family rentals are owned by small investors and mom-and-pop operators, while the publicly traded REITs only own ~1% of all single-family rental homes in the U.S.

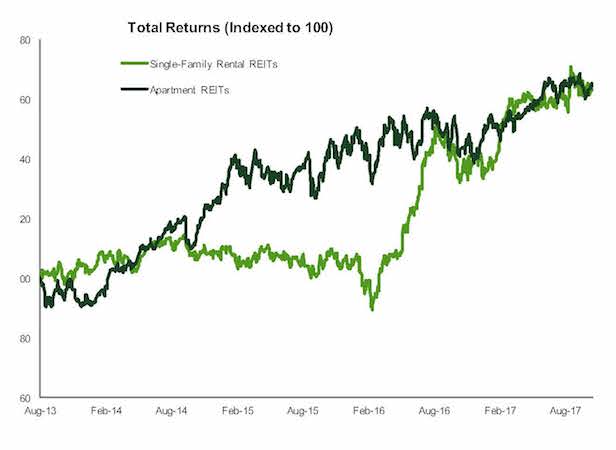

With a history of less than five years in the public-market, many mutual fund and hedge fund managers are still trying to understand the space. The initial public-market track record for the REITs was poor from mid-2013 through early 2016, when they began to dramatically improve operations. Big operators are proving they can control costs, improve margins and grow rents. The near-term operating outlook is favorable in absolute terms and relative to many other property types.

Improvements in expense and revenue management represent one of the biggest tailwinds for the sector. Ten years ago, the business would have been nearly impossible to operate without the technological tools used to support scaled operations in areas such as leasing and maintenance. The large public REITs and some smaller private operators (e.g., Progress Residential, Tricon American Homes) have made substantial investments in their platforms and management teams. These platform improvements have alleviated prior concerns from investors that management teams can successfully run this operationally-intensive business.

New single-family home construction remains below long-term average levels, and the minimal new supply is contributing to the favorable outlook for single-family rentals. In contrast, new construction starts in the apartment sector are well above the long-term average.

Starter single-family home construction activity, which represents the closer competing price point to the REIT portfolios (i.e., average home value of ~$250,000), is even more restrained. Fannie Mae and Freddie Mac are currently piloting inaugural initiatives in the space. Government-sponsored enterprise (GSE) involvement is positive for smaller operators and the REITs, as they offer access to less costly debt, and would ostensibly serve as a lender of last resort in times of economic distress.

Home price appreciation trends have been robust across most markets and are still rising, which is subsequently driving up the value of private and public single-family rental portfolios. For the REITs, operational efficiencies, attractive margins on acquisitions, and higher share prices have provided the currency to acquire additional homes and help mitigate the pressure from rising home prices. Time will tell if long-term home price appreciation trends will continue, and if rent growth will keep up with home prices.

Homeownership trends are also worth watching—though few industry participants acknowledge this risk. The homeownership rate had declined precipitously for the past 12 years, but recently the rate has stabilized and showed signs of a possible revival.

Although the 28- to 45-year-old age cohort is challenged by stretched consumer balance sheets and tighter lending, their appetite for owning a home has not diminished. The vast majority of single-family rental tenants would ultimately like to own their homes and if homeownership rebounds, increased move-out activity would pressure rent growth.

Though operating platforms have improved meaningfully from the sector's early-years, long-term capital expenditure requirements (“cap-ex”) remain a question mark for the space, given the short operating history. Today's reported capital expenditures are low due to the large rehab investments made upon acquisition, but the trajectory of cap-ex increases over time as the homes age remains an educated guess. Green Street expects long-term single-family rental cap-ex to be higher than multifamily.

The single-family rental sector has seen a flurry of consolidation activity over the last several years. The recent merger between Invitation Homes and Starwood Waypoint, though surprising upon announcement, makes sound strategic and financial sense. The portfolios overlap well together (80% of homes are in shared markets), and the merger will create significant value by likely removing nearly $50 million in costs from the platforms and combining the best management talent from both firms.

Public peer American Homes 4 Rent is expected to continue to expand aggressively in '18, and is likely to pursue larger portfolio acquisitions. Large private market players, including Progress Residential and Tricon American Homes, appear to be aggressively pursuing external growth as well.

The near-term single-family rental operating backdrop remains favorable, with superior growth in net operating income (NOI) versus most real estate sectors. The companies operating in this segment have done an impressive job building a business from scratch in fairly short order and proving out the operating story to public and private investors.

John Pawlowski is an analyst with Green Street Advisors, based in Newport Beach, CA. The views expressed here are the author's own.

NEWPORT BEACH, CA—The single-family rental sector, a newly institutionalized property type, is less well known and more fragmented than other sectors. The vast majority of single-family rentals are owned by small investors and mom-and-pop operators, while the publicly traded REITs only own ~1% of all single-family rental homes in the U.S.

With a history of less than five years in the public-market, many mutual fund and hedge fund managers are still trying to understand the space. The initial public-market track record for the REITs was poor from mid-2013 through early 2016, when they began to dramatically improve operations. Big operators are proving they can control costs, improve margins and grow rents. The near-term operating outlook is favorable in absolute terms and relative to many other property types.

Want to continue reading?

Become a Free ALM Digital Reader.

Once you are an ALM Digital Member, you’ll receive:

- Breaking commercial real estate news and analysis, on-site and via our newsletters and custom alerts

- Educational webcasts, white papers, and ebooks from industry thought leaders

- Critical coverage of the property casualty insurance and financial advisory markets on our other ALM sites, PropertyCasualty360 and ThinkAdvisor

Already have an account? Sign In Now

*May exclude premium content© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.