Freddie Mac headquarters

Freddie Mac headquarters

WASHINGTON, DC–Two separate offerings by Fannie Mae and Freddie Mac illustrate borrower demand for two types of loans: green and fixed-income, respectively.

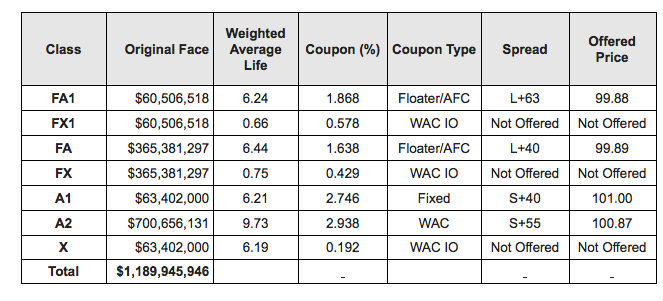

Last week Fannie Mae priced its eleventh Multifamily DUS REMIC in 2017 totaling $1.19 billion under its Fannie Mae Guaranteed Multifamily Structures program.

Three of the tranches — A1, A2 and X — were all backed by Fannie Mae's ten-year, fixed-rate green MBS collateral, according to Dan Dresser, vice president, Multifamily Capital Markets, Trading & Credit Pricing.

“This is Fannie Mae's third GeMS deal with a Green-only collateral group included,” he said in a prepared statement. “Strong interest from our traditional DUS investors and a new community of socially responsible investors helped to drive spreads tighter across the entire deal.”

Earlier this year Fannie Mae priced its first DUS REMIC with two green tranches. It was, according to the GSE, the first green agency CMBS deal. The beginnings behind that benchmark deal began several years ago when Fannie Mae began quietly and then not-so-quietly marketing its green MBS securities.

At the same time, the agency has been been rolling out various initiatives to encourage borrowers to make water and energy improvements to the GSE's asset base. Then last year some $3.5 billion in green MBS was issued. At that point the GSE had accumulated the critical mass to re-securitize the paper in its REMIC program and as this latest transaction shows, it continues to do well.

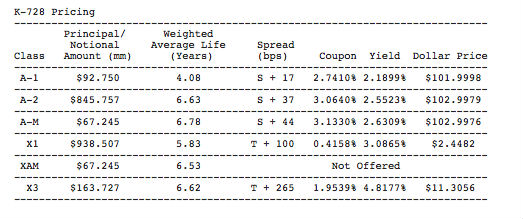

Separately, Freddie Mac priced a new offering of Structured Pass-Through Certificates, its vaunted K Certificates, backed by underlying collateral that consisted of fixed-rate multifamily mortgages with predominantly 7-year terms. The company expects to issue approximately $1 billion in K-728 Certificates, which are expected to settle on or about November 13, 2017.

For the most part the offering is business as usual. What is interesting is the seven-year, fixed rate paper. To be sure fixed-rate offerings have been a staple of the GSEs. But it is becoming clear that the fixed rate loans are more in favor than the floating rate loans this year. There are likely many reasons for that with the rise in Libor and the maturity of the cycle chief among them.

Want to continue reading?

Become a Free ALM Digital Reader.

Once you are an ALM Digital Member, you’ll receive:

- Breaking commercial real estate news and analysis, on-site and via our newsletters and custom alerts

- Educational webcasts, white papers, and ebooks from industry thought leaders

- Critical coverage of the property casualty insurance and financial advisory markets on our other ALM sites, PropertyCasualty360 and ThinkAdvisor

Already have an account? Sign In Now

*May exclude premium content© 2025 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.

Erika Morphy

Erika Morphy has been writing about commercial real estate at GlobeSt.com for more than ten years, covering the capital markets, the Mid-Atlantic region and national topics. She's a nerd so favorite examples of the former include accounting standards, Basel III and what Congress is brewing.