Multifamily’s New Math

The apartment asset class is having a numbers problem with deals and development getting harder to pencil in. Still, the fundamentals are strong enough to withstand these issues.

{kind=link}

What will it take for the seemingly indefatigable multifamily asset class to lose steam? Slowing rent growth? Apparently not as many, if not most, markets have experienced a deceleration in rent growth. Too much supply? Again, that would be no. While the volume of apartment development may seem overwhelming on a macro basis it still falls short of housing demand.

Instead, what investors in this space are more fearful of is the interest rate environment, with a whopping 70% of respondents to a Real Capital Markets survey declaring that the prospect of further increases is having, and will have in the future, an impact on acquisition strategies.

Vic Clark, senior managing director for Hunt Real Estate Capital, notes that interest rates have moved up about 60 basis points over the past year. “In the past 12 to 18 months, lending agencies have found ways to reduce pricing and keep rates low despite interest rate hikes,” he says. “So far, cap rates have held firm, but another 60-basis-point rate increase will be difficult to absorb.”

As it happens, the multifamily sector will probably navigate that issue as well. Its fundamentals are too strong to ignore.

{kind=link}

“Things seem to be picking up,” observes Tina Lichens, chief operating officer, Real Capital Markets. According to company data, multifamily sales volume for the US was $69.8 billion for the first half of 2018, a 7.7% year-over-year increase. Furthermore, more than half of the investors surveyed in July now consider themselves net buyers, while another 26% want to remain in a holding pattern. Just 16% consider themselves net sellers. “The challenge for many investors is finding quality assets at reasonable prices,” Lichens says.

A STEP UP FROM ELEMENTARY

That said, it is equally clear that multifamily’s math is no longer so simple.

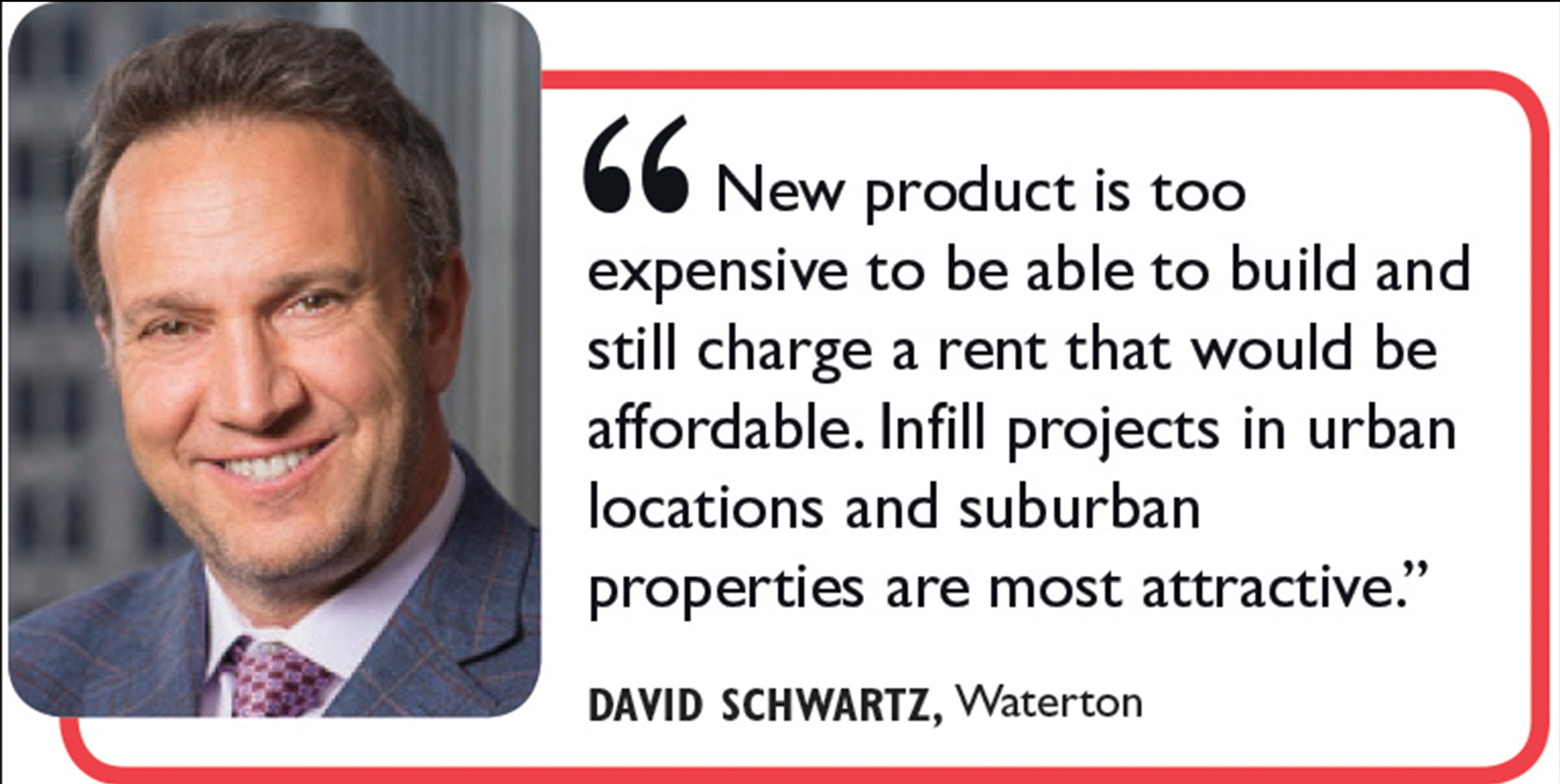

Investment pricing, for example, is seeing significant swings from market to market. “There is a vast spread in pricing,” says David Schwartz, CEO, chairman and co-founder of Waterton. In New York, for example, he says that it is challenging for owners to sell property because they won’t like where the assets will trade. “Expense growth is outpacing rent growth and there is a supply issue.”

And even that old standby for the market—the value add play—is becoming harder to pencil in. “Today, buyers are more selective in the upgrades and improvements they make to a new acquisition and are less likely to complete a total rehab,” says John Sebree, first vice president and national director of Marcus & Millichap’s National Multi Housing Group. ”Most look to reposition a property by improving common areas (clubhouse, landscaping, signage) and interiors (kitchen countertops, flooring, fixtures) with the intent to upgrade a B-quality asset to an A- quality asset.”

{kind=link}

Developers have their own issues as well even as demand for new product remains unabated. All of the activity is straining labor markets and supply chains, pushing up construction costs, which are further compounded by the price of steel and aluminum tariffs, according to Tara Hovey, president and COO of Optima Inc., a family-owned real estate firm that achieves total quality control by serving as architect, developer, general contractor, and property manager or sales broker for its multifamily rental and for-sale projects in the Chicago area and Arizona.

“The market is facing a capacity issue as there are limits on the availability of some trade labor,” Hovey adds, “which without solid teams in place can affect construction schedules.” In addition, she notes that scarcity of quality land sites also is impacting development, as developers look to secure property at the right price to make financial sense of a potential transaction.

A STRONG FOUNDATION

Despite these issues, virtually no one expects the sector to register significant difficulties.

“Overall, the market remains strong with significant capital, both domestic and foreign, looking to be placed,” says Real Capital Markets’ Lichens. The multifamily market is indeed the ultimate defensive play–after all, everyone needs a place to live.

In fact, they need a place to live more than ever before in US history. Millennials and other demographic groups continue to forego homeownership in favor of renting in walkable neighborhoods. “The continued strength of the national economy has aligned with the wave of Millennials in their late 20s moving into their first independent residence,” Sebree says.

At the same time, available housing supply over the past few years has drawn down, creating shortages. Also, young adults are finding the option of homeownership increasingly challenging, reinforcing the need for more apartments.

{kind=link}

It should be said that this shift to renting over home ownership could reverse again as Millennials now, and later on, Generation Z create their own families. “Millennials watched their families live through the financial crisis and, as a result, created a paradigm shift from homeownership to rental,” says Dan Slack, principal at Baker Development Corp. “Now, they are maturing in their thought process and financial position, allowing them for the first time to consider homeownership.”

BALANCING THE UNDERLYING EQUATION

None of this is to say that multifamily’s pipeline is in equilibrium. It has, in fact, a troublesome oversupply problem, especially in some markets. The bigger point, many argue, is that these will work themselves out as demand shows no sign of abating. “The pipeline can reasonably be described as a flood and though demand for these units is likely to come in the years ahead, we can expect to see some significant digestion issues in the near term,” relates Peter Muoio, a senior economist with Ten-X.

The overall housing supply will need to increase to keep pace with demand, Sebree concludes.

One reason the short-term may not be so pretty for apartment owners is that influx of supply has led to a dampening of rental growth. Year-to-date rent growth has been about 3%, according to Yardi Matrix. That is down significantly from the 5.2% growth seen in the third quarter of 2015, and some analysts see it dropping even further.

A recent Ten-X report forecasted that rent growth will continue to cool reaching the low 2% range in 2021. And 65% of survey respondents in the Real Capital Markets multifamily report also found the outlook for rent growth to be marginal. “Even in markets like Washington, DC, you’ve had tremendous absorption, but not a lot of rent growth,” indicated Alan George, executive vice president and chief investment officer at Equity Residential, in the report.

Much of course depends on the market and the apartment category. Sebree, for example, notes that class A performance has softened in some metros, resulting in increased concessions and little to no year over year rental increases. But class B and C vacancies are at lower levels than any time in recent history. “As demand for workforce housing continues to increase and wage growth improves, this sector of the multifamily market remains poised for steady gains going forward,” he says.

INVESTORS’ MULTIPLE CHOICES

Investors are well aware of these short and long-term dynamics and are placing their money according to how they feel the market will play out. The value add space, for example, has proven to be very popular—perhaps too popular, some might say.

“This market segment remains strong but is experiencing intense competition and now a scarcity of supply in many markets,” Real Capital Analytics’ multifamily report says. “There is considerable demand for properties from the 1970s, ’80s and ’90s, where investments can be made to improve the aesthetics, the common areas and units.”

{kind=link}

The category, though, still has its fans. Waterton’s David Schwartz says that from an investment perspective, all-in cost for a value-add investment is still better than replacement cost and there is great demand for apartment and amenity packages that are consistent with new product. “New product is too expensive to build and still charge a rent that would be considered affordable,” he says. “There are plenty of affordable properties in very replicable locations, but it’s the infill projects in urban locations and suburban properties that are most attractive to us.”

Tyler Anderson, a vice chairman of institutional properties with CBRE in Phoenix, adds that a similar theme can be seen in his own market. “With some 1,100 older properties that have 100 or more units, there are always properties well suited for repositioning and a value-add approach,” he observes.

Essentially, according to Clark, there is a lot of competition for value-add properties and you may have to look hard, but you can find them. “There is always somebody who bought the property 10 years ago and wants to sell. You can come in and spend $1 million to upgrade the units and get a lot of pop and return on that investment.”

On the other end of the spectrum, many investors and builders have sought out the luxury segment to deliver their much-needed yields. “Millennials, Gen-Xers and baby boomers are seeking luxury multifamily communities with state-of-the-art amenities that meet—even exceed—their expectations,” says Hovey. And with unemployment at historically low levels, economic dynamics bode well for the luxury sector. “The only cautionary note,” she warns, “is whether wage growth and the depth of the market can keep pace.”

SIDEBAR | Mapping the Top Buy-Sell Markets

A US Apartment Market Outlook released by Ten-X Commercial showed a US multifamily market grappling with robust supply as vacancies have climbed 40 basis points in the past year and are projected to soar by another 110 basis points by 2021.

Completions have outstripped absorption for six straight quarters, while absorption has slipped to its lowest level in more than five years, noted Peter Muoio, the firm’s chief economist. “While today’s sub-5% vacancy rate is relatively low from a historical perspective, vacancies have climbed to their highest level since 2012 amid this new supply,” he says.

The report identifies Houston, Raleigh-Durham, NC, Salt Lake City, Fort Worth and Charlotte, NC as the top markets in which investors should consider buying multifamily assets. These markets continue to enjoy significant demand, which is underpinned by resilient local economies.

Rich Sarkis, CEO of Reonomy, seconded that Salt Lake City is worth taking a second look as the city’s ongoing transformation into a bonafide tech hub should excite commercial real estate investors, especially those primed to take advantage of the city’s expanding office and multifamily housing markets.

Simply put, he said, as new residents flock to Salt Lake to satisfy companies’ ever-increasing demand for top-notch talent, they’re going to need places to live.

Miami, San Jose, New York City, San Francisco and Oakland, CA are the top markets where conditions might cause investors to consider selling multifamily properties, notes the Ten-X report. These cities, the report says, “face rising vacancies and flattening rents as a wave of new supply is hitting the market—a situation which has not improved in the past six months and shows no signs of abating.”

According to David Schwartz, CEO, chairman and co-founder of Waterton, as demand generation is tightly correlated with job creation, job growth and the ability to create jobs are overarching themes that make a market more attractive for buying and selling. “A deep talent pool and irreplaceable assets that attract multi-national companies are also attractive for multifamily investors.”

He notes that Waterton also believes in markets with a workforce that doesn’t rely on one employer or employment sector. “Even Houston, which had been reliant on energy in recent years, has diversified. Nashville is a market that, five years ago, we would not have pursued, but it has become liquid with a diversified employment base.”

Lastly, he says, markets that see capital flow and liquidity through all points in the cycle are most appealing for multifamily investment. “High barriers to entry with regard to cost and entitlements also make markets attractive for buying and selling. For example, in Dallas there are some areas where it’s hard to build, but, we just bought three properties in Plano, just 20 miles north of Dallas, and even though it’s tough to build, there’s strong job growth in and around Dallas. It’s a large market that offers liquidity through all the cycles.”

SIDEBAR | A Different Kind of Logic Behind Rising Interest Rates

Respondents to recent Real Capital Markets survey were very specific about their qualms for the multifamily market: rising interest rates could have an effect on pricing and valuations. But some argue that rising interest rates are not a major risk for this asset class.

On a national level, it’s almost a non-issue, according to Dan Slack, principal at Baker Development Corp. “Long-term interest rates are benchmarked off of the 10-year US Treasury, which has been hovering at less than 3% in spite of the recent hike in the Federal Funds rate,” he relates. “I expect this trend to continue as the US economy is just hitting its stride and, as a result, the 10-year Treasury is still considered the safe-haven to the global investment community.”

A cooling of the economy will undoubtedly curtail construction spending increases as well as land speculation, he adds, but will also drive 10-year Treasury yields even lower. This, Slack explains, is because a slowdown in the US economy will undoubtedly be followed by, or in concert with, a global slowdown and the 10-year T-bill will be viewed even more safe.

“From a contrarian standpoint, however, rising interest rates don’t necessarily need to be viewed negatively as but for rare instances, they are typically the result of a healthy economy.”