The Retail Issue | Marcus & Millichap Retail Trends: Mapping The Changes In Retail

Since 1971, Marcus & Millichap has provided the commercial real estate industry with a multitude of investment services. As a leader in the private…

{kind=link}

Since 1971, Marcus & Millichap has provided the commercial real estate industry with a multitude of investment services. As a leader in the private client market segment, which comprises approximately 80 percent of all commercial property sales, Marcus & Millichap is the nation’s most active commercial real estate firm focused on brokerage and financing. The firm’s industry-leading Net Leased Properties Group and National Retail Group are major influencers in the retail commercial property sector. Scott M. Holmes, Marcus & Millichap senior vice president and national director, retail leads both divisions.

Blending of Online and In-Store Retail

{kind=link}

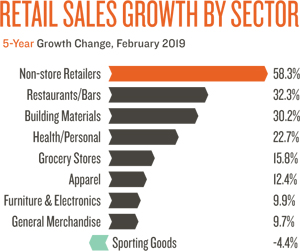

Retail Categories that are Thriving

{kind=link}

{kind=link}

{kind=link}

Retail Categories that are Struggling

{kind=link}

{kind=link}

The new age of retail has prompted companies to reevaluate their business models. High-inventory layouts are no longer effective as showroom-style concepts provide more economic value and cater more closely to current consumer preferences. With many department stores continuing to operate with an outdated model, sales have taken a hit, falling 12 percent over the past five years. The closing of many department store chains has left numerous malls unanchored, forcing owners to creatively fill empty space. Sporting goods stores have also struggled to evolve with the retail landscape. Several of these retailers, while popular as showrooms where consumers can test products before they buy, have difficulty offering prices that effectively compete with online marketplaces. This has thinned the sporting goods playing field, leaving only chains with the most sophisticated omnichannel platforms.

{kind=link}

Why Retail is Gaining Despite Record Store Closings

{kind=link}

Retail Embracing Technology Faster than Other Industries

{kind=link}

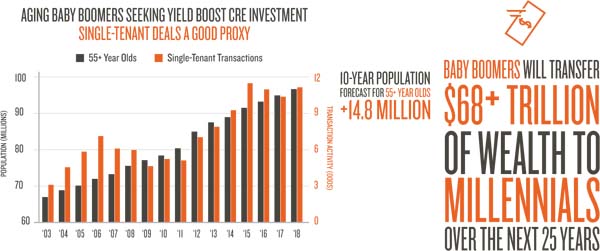

Baby Boomers Look to Single Tenant Net Lease as Strategic Investment

{kind=link}

{kind=link}

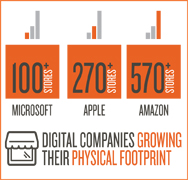

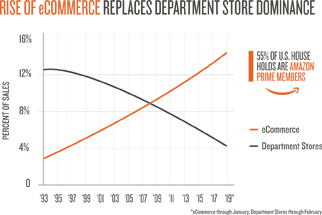

Retail has evolved past the idea that either online or brick-and-mortar stores will survive, as both sides move closer to an omnichannel concept. A growing number of digitally native brands are stepping into brick-and-mortar locations as they realize the effect physical stores can have on their bottom line. Online startups including Bonobos, UNTUCKit and Warby Parker are aggressively opening stores, while tech heavyweights Amazon, Apple and Microsoft also place an emphasis on their physical footprints. Conversely, brick-and-mortar retailers are quickly growing their digital infrastructure to achieve stronger omnichannel models. Walmart and Home Depot have considerably increased their online presence, making them close competitors with some well-established e-tailers.

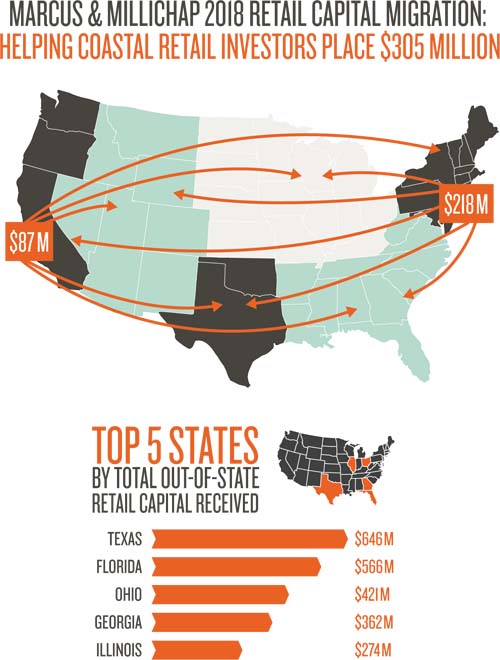

Migration of Capital

As the business cycle has matured, investors have utilized portfolio diversification strategies and interstate capital flows to boost returns. The Sunbelt remains the focus of investment as many markets in this region are experiencing high growth, providing opportunities to a number of buyers. Yield-driven investors have been more focused on locations throughout the Midwest, where buyers pursue cap rates well above the national average. Major coastal cities remain the primary sources of capital as extremely large populations and deep financial services markets provide both institutional and private clients access to multiple opportunities. Additionally, cap rates in these markets remain very tight, encouraging buyers to undertake strategies to enhance the yield in their portfolios.

{kind=link}

The Fundamentals

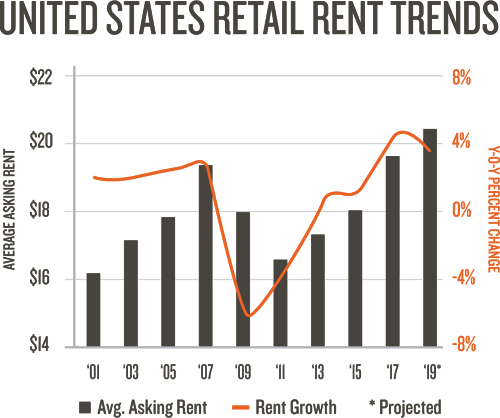

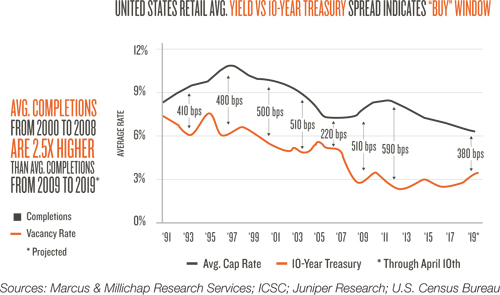

The retail sector has made significant gains since the last recession, with multi-tenant vacancy dropping below 6 percent and rents nearing prerecession highs. Tapered-back construction efforts have supported improving fundamentals as developers and lenders have taken caution after vastly overbuilding in the last business cycle. During that span, annual retail completions averaged 150 million square feet, whereas the current expansion features just over 50 million square feet of new space each year. Single-tenant retail comprises most deliveries; however, the share of multi-tenant space has substantially risen each of the past two years. This points to higher developer confidence in the direction of the retail sector as omnichannel models become the standard.

{kind=link}

{kind=link}

{kind=link}

Sources: Marcus & Millichap Research Services; ICSC; Juniper Research; U.S. Census Bureau Analysis and commentary for this feature was provided by Marcus & Millichap’s national director of retail, Scott M. Holmes, and Marcus & Millichap Research Services. Additional information collected from Marcus & Millichap Research Services, U.S. Census Bureau, The Heartman Group, Pew Research, Morgan Stanley, IHL Group, CoStar Group, Inc., Real Capital Analytics, Moody’s Analytics, Federal Reserve, Cerulli Associates.