Heighten Volatility Expected in Months Ahead in Capital Markets

The index of leading indicators appears to show that capital markets are moving beyond the devastation of the coronavirus.

Heightened volatility appears to be causing dramatic swings in the American financial markets. In the months ahead, investors and central banks will have to mitigate the damages caused by the coronavirus, the ensuing economic shutdown, and look forward to the impact of the upcoming elections, according to a new report by BentallGreenOak.

The index of leading indicators, which signals turning points in the economy, appear to show that capital markets are moving beyond the devastation of the coronavirus. February marked the end of the US expansion, with severe job losses and the country entering into a recession only a few months later. Now, major US stocks have rebounded from the COVID-19 shock with the S&P 500 turning positive for the year.

The shift in sentiment has been dramatic since late March when investors fled both stocks and bonds and moved to cash as cases of the coronavirus spiked. BentallGreenOak attributed the turnaround to low-interest rates, unprecedented actions by the Federal Reserve, fiscal stimulus, positive news about the coronavirus treatment options, and the reopening of the economy.

Globally, investors have reaffirmed their view of the U.S. economy as a safe haven for assets. For instance, since February, the US 10-year bond yield has fallen below those of higher-risk countries, such as Italy and Greece.

But without a vaccine for the coronavirus, the uncertainty for both the elections in November and the ongoing trade was with China, Bentall Green Oak is expecting the market to have significant volatility in the weeks and months ahead.

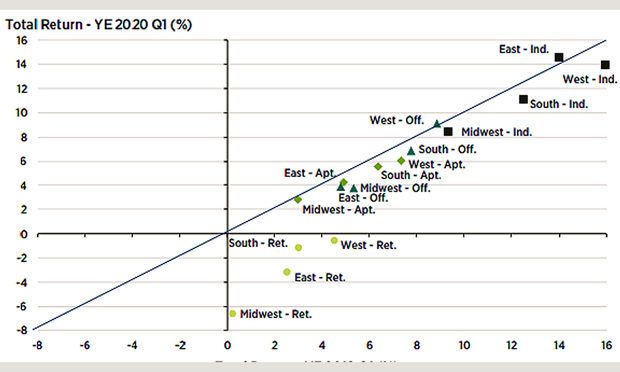

That is evident in investment performance, which is showing symptoms of the coronavirus. For example, national returns, as measured by the NCREIF Property Index, have lost momentum across sectors. The index provides a measure of investment performance for a large pool of individual commercial real estate properties acquired in the private market.

{kind=link}

Compared to a year ago, commercial real estate investment performance has declined while investment activity has stalled. By region, only the east industrial and west office had higher returns over the past four quarters than they did over the previous quarters. To no surprise, industrial outperformed across all the regions. At the same time, retail returns turned negative in all four regions.

Returns will likely continue its descent as property net operating income will continue to erode, and some investors remain cautious. But, the low-interest-rate environment should benefit property values, adding as a cushion to the battered sector to prevent a stronger downside descent.