Brian Sykes: “Millennials are a lot slower in homeownership,” says Brian Sykes, the Boston-based SVP of Capital One.

Brian Sykes: “Millennials are a lot slower in homeownership,” says Brian Sykes, the Boston-based SVP of Capital One.

NEW YORK CITY—It's going to happen at some point, the Millennial generation will eventually want families and settle down, presumably renouncing their live/work/play lifestyles for houses they own with picket fences and mortgages. What then of the CBD revitalization they're so often credited as driving? For that matter, is the assumption of homeownership even accurate? The short answer is that there is no short answer. Experts we talked with say there's more at play here than graying hair and the ability to afford a house.

Indeed. Homeownership is on the decline for Millennials, grouped in the 25- to-30-year-old category by Dallas-based Axiometrics. The firm's senior real estate economist, KC Sanjay, tells GlobeSt.com that 12.1% of Millennials were homeowners in 2000. By 2005 that number had slipped to 11.5%, and to 9.8% five years later. The estimate for year-end 2015 is 8.5%. That includes condo ownership.

Projecting that out, then, would build a good case for the continuation of the rental trend—in both the CBD and in suburban town centers. “Millennials are a lot slower in homeownership,” says Brian Sykes, the Boston-based SVP of Capital One. Not only are the prices out of reach, but that youthful cohort is “more likely to move around a lot more in their jobs. Renting allows them that flexibility.”

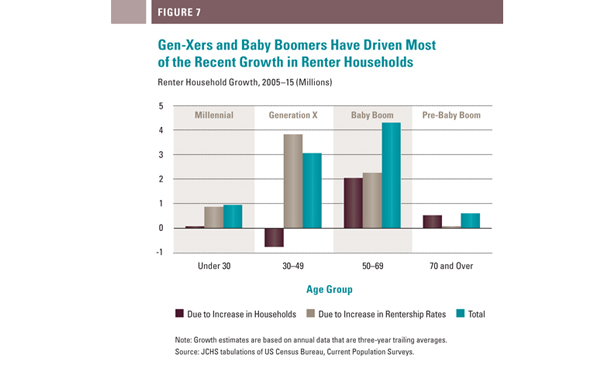

Defining Millennials as people from 18 to 34 years old, Caitlin Walter, director of research for the Washington, DC-based National Multifamily Housing Council, quotes a recent Harvard study that supports the case for sustainability of the rental trend. “The study says that, over the next decade—if homeownership rates remain the same—the number of Millennial renters will double from 11 million today to 22.6 million,” she says. “The subsequent generation—after Millennials—will add another 500,000 new households to the ranks of renters. It certainly shows us that renting fundamentals are still good going forward.”

Conducted by Harvard's Joint Center for Housing Studies, the study indicates that renting is becoming more common across many age groups—including the oft-forgotten Baby Boomer set.

The Big Rental Picture

No matter the age, financing is available to meet this rental surge. The majority of respondents to NMHC's October 2015 Quarterly Survey of Apartment Conditions indicate that equity financing for apartment acquisition or development is roughly unchanged from the quarter before, neither less nor more available.

“There are a lot of funds with a lot of pressure to get money out,” adds Sykes. So much so, in fact, that it's trickling out to “secondary and tertiary markets, for both acquisition and development.”

Respondents also stated that conditions for multifamily mortgages were also unchanged. But, according to Sykes, “That depends on where you are. If you're in a highly competitive market, let's say the Northeast or West Coast, there's a tremendous amount of competition, be it regional banks, the agencies or life companies. Therefore, the pricing is incredibly competitive, and to an extent, the underwriting is getting a little aggressive.” Nothing, he adds, like 2006 or 2007, but aggressive nonetheless, especially on the coasts.

Courtesy Harvard's Joint Center for Housing Studies

Courtesy Harvard's Joint Center for Housing Studies

Build Here, Revamp There

At this point in the cycle, says Paul Nasser, CFO and COO of Boston-based Intercontinental Real Estate Corp., his firm's focus in CBDs is on ground-up construction. “We can get a little more return if we take a little more risk on the development and lease-up,” he says. Nasser has found that 60% of renters in those buildings are either Boomers or Millennials, and “probably 50% of our CBD buildings are filled with Millennials.”

In the suburbs, the play for Intercontinental switches to value-add, typically properties with good transportation and walkability to local amenities—features that appeal to Boomers and Millennials alike. “We can go in and do a $6,000 to $10,000 spend per unit, increase the rents commensurate with that spend and still maintain a differential from the CBD that would attract the different populations—both Millennials and dual-income earners with or without kids,” he says.

Sykes agrees. “There's a tremendous push on suburban value-add at this point,” he says, “more than is taking place in the CBDs.”

But Is It Sustainable?

In terms of sustainability, Nasser says that's largely a matter of local market conditions as much as sociology. “Now you're hitting on the big question,” he says. “There's been a tremendous amount of development, whether it's ground-up or renovation of older stock. At what point do we meet market demand? There are some cities where they're approaching more than enough units being built to support the demand.” He cites his own backyard—Boston—as one city that could max out.

But on the sociological side, he's not quick to assume that once Millennials start their families, they'll abandon the CBD for the suburbs simply because that's what families do. The big variable here is the school district.

“There's a huge movement in most major cities to upgrade their educational offerings,” says Nasser, “whether in charter schools or private schools or more expenditure on the public side. If cities can make their school systems viable, that would make an interesting decision for Millennials. They like the city lifestyle, and the parents have come to the city to be near them. So are they comfortable in a city school?”

Sykes agrees that the potential for cities to upgrade their schools could be a real game-changer in the CBD/suburban dynamic for Millennials. But, even if that cohort leaves the city for the 'burbs, they're more likely to rent than buy. “They're looking for a better work/life balance and would rather opt for a smaller apartment and be closer to work than for a large suburban home and a long commute.”

It's a projection that bodes well, he says, for suburban apartment communities and town centers. At least for now.

Brian Sykes: “Millennials are a lot slower in homeownership,” says Brian Sykes, the Boston-based SVP of

Indeed. Homeownership is on the decline for Millennials, grouped in the 25- to-30-year-old category by Dallas-based Axiometrics. The firm's senior real estate economist, KC Sanjay, tells GlobeSt.com that 12.1% of Millennials were homeowners in 2000. By 2005 that number had slipped to 11.5%, and to 9.8% five years later. The estimate for year-end 2015 is 8.5%. That includes condo ownership.

Projecting that out, then, would build a good case for the continuation of the rental trend—in both the CBD and in suburban town centers. “Millennials are a lot slower in homeownership,” says Brian Sykes, the Boston-based SVP of

Defining Millennials as people from 18 to 34 years old, Caitlin Walter, director of research for the Washington, DC-based National Multifamily Housing Council, quotes a recent Harvard study that supports the case for sustainability of the rental trend. “The study says that, over the next decade—if homeownership rates remain the same—the number of Millennial renters will double from 11 million today to 22.6 million,” she says. “The subsequent generation—after Millennials—will add another 500,000 new households to the ranks of renters. It certainly shows us that renting fundamentals are still good going forward.”

Conducted by Harvard's Joint Center for Housing Studies, the study indicates that renting is becoming more common across many age groups—including the oft-forgotten Baby Boomer set.

The Big Rental Picture

No matter the age, financing is available to meet this rental surge. The majority of respondents to NMHC's October 2015 Quarterly Survey of Apartment Conditions indicate that equity financing for apartment acquisition or development is roughly unchanged from the quarter before, neither less nor more available.

“There are a lot of funds with a lot of pressure to get money out,” adds Sykes. So much so, in fact, that it's trickling out to “secondary and tertiary markets, for both acquisition and development.”

Respondents also stated that conditions for multifamily mortgages were also unchanged. But, according to Sykes, “That depends on where you are. If you're in a highly competitive market, let's say the Northeast or West Coast, there's a tremendous amount of competition, be it regional banks, the agencies or life companies. Therefore, the pricing is incredibly competitive, and to an extent, the underwriting is getting a little aggressive.” Nothing, he adds, like 2006 or 2007, but aggressive nonetheless, especially on the coasts.

Courtesy Harvard's Joint Center for Housing Studies

Build Here, Revamp There

At this point in the cycle, says Paul Nasser, CFO and COO of Boston-based Intercontinental Real Estate Corp., his firm's focus in CBDs is on ground-up construction. “We can get a little more return if we take a little more risk on the development and lease-up,” he says. Nasser has found that 60% of renters in those buildings are either Boomers or Millennials, and “probably 50% of our CBD buildings are filled with Millennials.”

In the suburbs, the play for Intercontinental switches to value-add, typically properties with good transportation and walkability to local amenities—features that appeal to Boomers and Millennials alike. “We can go in and do a $6,000 to $10,000 spend per unit, increase the rents commensurate with that spend and still maintain a differential from the CBD that would attract the different populations—both Millennials and dual-income earners with or without kids,” he says.

Sykes agrees. “There's a tremendous push on suburban value-add at this point,” he says, “more than is taking place in the CBDs.”

But Is It Sustainable?

In terms of sustainability, Nasser says that's largely a matter of local market conditions as much as sociology. “Now you're hitting on the big question,” he says. “There's been a tremendous amount of development, whether it's ground-up or renovation of older stock. At what point do we meet market demand? There are some cities where they're approaching more than enough units being built to support the demand.” He cites his own backyard—Boston—as one city that could max out.

But on the sociological side, he's not quick to assume that once Millennials start their families, they'll abandon the CBD for the suburbs simply because that's what families do. The big variable here is the school district.

“There's a huge movement in most major cities to upgrade their educational offerings,” says Nasser, “whether in charter schools or private schools or more expenditure on the public side. If cities can make their school systems viable, that would make an interesting decision for Millennials. They like the city lifestyle, and the parents have come to the city to be near them. So are they comfortable in a city school?”

Sykes agrees that the potential for cities to upgrade their schools could be a real game-changer in the CBD/suburban dynamic for Millennials. But, even if that cohort leaves the city for the 'burbs, they're more likely to rent than buy. “They're looking for a better work/life balance and would rather opt for a smaller apartment and be closer to work than for a large suburban home and a long commute.”

It's a projection that bodes well, he says, for suburban apartment communities and town centers. At least for now.

Want to continue reading?

Become a Free ALM Digital Reader.

Once you are an ALM Digital Member, you’ll receive:

- Breaking commercial real estate news and analysis, on-site and via our newsletters and custom alerts

- Educational webcasts, white papers, and ebooks from industry thought leaders

- Critical coverage of the property casualty insurance and financial advisory markets on our other ALM sites, PropertyCasualty360 and ThinkAdvisor

Already have an account? Sign In Now

*May exclude premium content© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.

John Salustri

John Salustri has covered the commercial real estate industry for nearly 25 years. He was the founding editor of GlobeSt.com, and is a four-time recipient of the Excellence in Journalism award from the National Association of Real Estate Editors.